At a glance

- Unpredictable sales and rising costs are making it harder for NZ retailers to manage day-to-day cash flow.

- Small shifts, like smarter pricing or leaner inventory, can free up capital and create space to grow.

- With the right tools and retail funding support, small stores can stay resilient and expand without overcommitting.

For many small retailers in New Zealand, the rhythm of trading has become harder to predict. Sales are softer, customers more cautious, and costs continue to climb. RNZ reports that total retail sales in 2024 fell by 2.2% compared to the previous year.

In 2025, staying afloat often takes priority over scaling up. But with the right strategies, it’s possible to do both. This article offers practical, real-world advice tailored for NZ retailers on managing inventory and pricing, exploring low-risk expansion, retail funding options, and more.

Why cash flow keeps catching small retailers off guard

NZ retailers are juggling a mix of challenges that make cash flow harder to manage. Rising costs, cautious consumer spending and smaller basket sizes are putting pressure on even well-run businesses.

For many, these issues often stay hidden until they escalate. A busy sales month might still leave little in the bank. Stock can sit unsold, while supplier or staffing costs quietly rise. Steadfast NZ notes that the average small business experiences negative cash flow for four months of the year — and 17% for more than six.

Common pressure points include:

- Capital tied up in slow-moving inventory

- Late payments from customers or wholesale partners

- Margin squeeze from rising supplier, wage or overhead costs

When these challenges build, cash flow starts driving every decision: what to stock, how often to restock and whether the business is in a position to grow.

Cash flow tactics NZ retailers can rely on

With cash flow under pressure, the key is to know where your money’s tied up, and take action early.

Here are six practical tactics NZ retailers can use to stay in control:

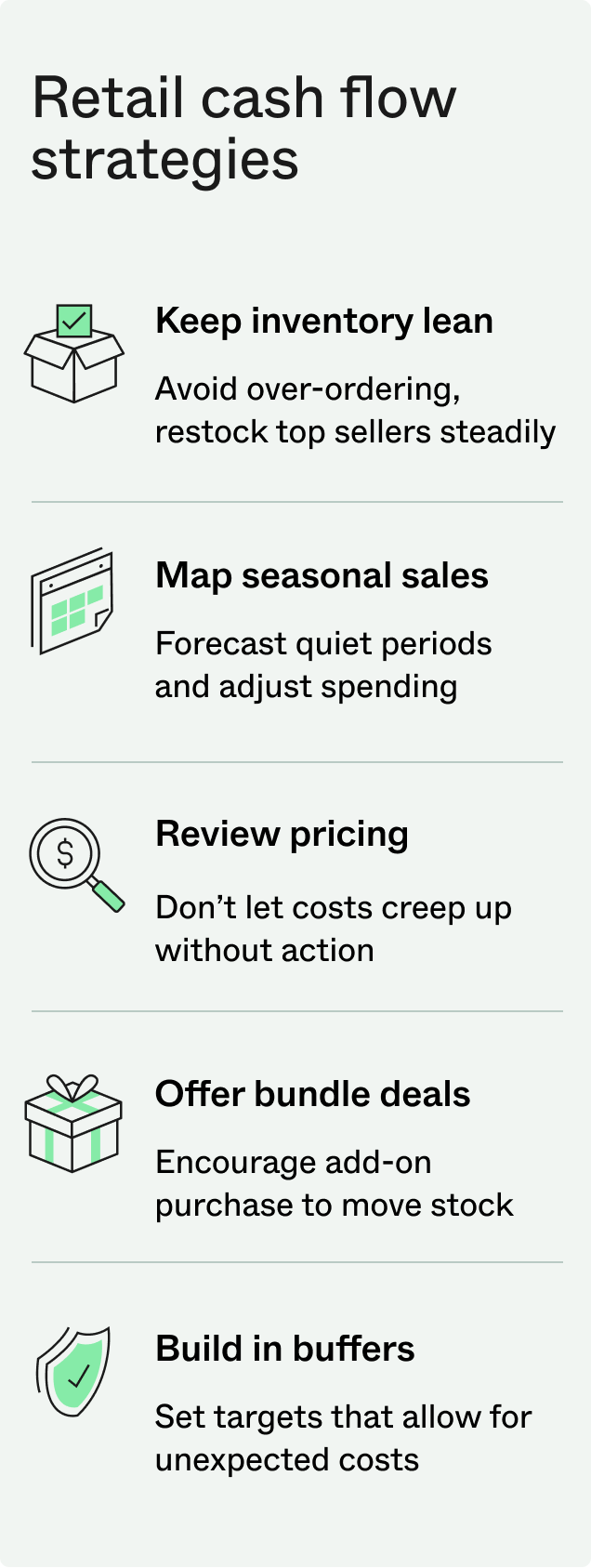

1. Keep inventory lean and responsive

Avoid tying up capital in stock that doesn’t move. Use POS data to track bestsellers, and only restock when items are trending steadily. Trial new products in small batches before committing.

2. Plan based on seasonal sales patterns

Use past sales data to forecast slow periods and busy stretches. Overlay holidays, weather trends or local events to adjust orders, rosters and promotions. Use a simple spreadsheet or forecasting tool to adjust inventory orders, staffing and marketing spend before sales dip.

3. Review pricing and margins regularly

Even small cost increases from suppliers can eat into your profit. Revisit your pricing at least quarterly, especially on popular items. Consider adding perceived value, like gift wrapping or samples, instead of defaulting to discounts.

4. Refine your retail store strategy

Where and how products are displayed affects how quickly they sell. Make high-margin or in-demand items easier to find, and rotate displays to reflect the season or any current promotions.

5. Use bundles and small incentives to shift stock

Rather than relying on blanket sales, group slow-moving items with popular ones or offer a gift-with-purchase to shift excess inventory. Tools like Shopify’s bundle apps or in-store POS promotions make this easy to roll out.

6. Build in cash flow buffers where you can

When setting your monthly targets, include a cushion for late payments, surprise costs or delays in inventory delivery. A basic four to six week rolling forecast, even in Excel, can help you spot shortfalls before they happen. You can also create a simple cash reserve to give your business more breathing room when things are quiet or unpredictable.

Growth strategies that won’t stretch your cash flow

Once you’ve got a handle on cash flow, growth becomes the next focus. But that doesn’t mean spending big. The best retail business strategies often come from doing more with what you’ve already got, improving margins, reaching more customers, and building loyalty.

Here are a few low-risk ways to grow:

- Trial new products in small batches. Instead of launching a full range, start with a handful of SKUs and see what sells. Use POS and customer feedback to decide what’s worth expanding.

- Team up with another local business. It could be as simple as a bookshop working with a local café, or a gift store showcasing handmade ceramics from a nearby maker. Collaborations like these can boost foot traffic, create more value for customers, and even help share marketing costs.

- Keep your marketing focused. Highlight new arrivals or local partnerships on social media, through email, or with simple in-store signage. These small, steady efforts often outperform more expensive campaigns.

- Make the most of the checkout. In-store or online, suggest complementary products or create bundles to lift the average spend. Train staff to suggest related items, or use your ecommerce platform to recommend bundles based on browsing or purchase history.

- Start selling online in a targeted way. You don’t need a full-blown ecommerce setup to reach more people. A curated online store or a presence on a marketplace can help drive extra revenue without draining resources. These ecommerce tips can help you get started.

- Give customers a reason to return. A loyalty program isn’t always necessary. Personal touches, small surprises or thank-you notes can go a long way in building repeat business.

When funding makes sense for small retailers

Even the most careful retailers can hit a point where cash flow alone isn’t enough to support growth. A seasonal spike, an unexpected opportunity, or a large order might need upfront capital. In these moments, the right funding can help you move forward without putting the business at risk.

Here’s how to approach it:

- Get clear on your goal. Maybe you’re preparing for a peak season, planning a small fit-out or covering the upfront cost of a new product range. Having a specific plan makes it easier to choose the right option and stay focused on your return.

- Choose funding that fits your business model. A short-term retail business loan might be right for one-off investments or supplier payments. For more flexible access to funds, a Prospa Line of Credit gives you ongoing access up to your approved limit, so you can draw down what you need, when you need it, and only pay interest on what you use.

- Make sure repayments suit your cash cycle. If income fluctuates month to month, look for funding that gives you breathing room during slower periods. Avoid repayment plans that might tighten your cash flow when things get quiet.

- Use tools to make informed decisions. Before applying for funding, take stock of where your business stands. A quick check with the Prospa Loan Calculator can help you estimate repayments and model different scenarios before you commit.

- Ask questions and compare options. Not all funding is created equal. Look at approval speed, fees, flexibility and the support available to make sure it’s right for your retail business.

Need help weighing it up? A Prospa specialist can help you decide what makes the most sense for your retail business.